Cash vs. Accrual Accounting for Dental Practices: What’s the Difference?

March 2026 · 8 min read

If you own a dental practice, you’ve probably heard the terms “cash basis” and “accrual basis” thrown around by your CPA, your bookkeeper, or somewhere online. Most practice owners have a general sense that one is simpler and the other is more detailed—but beyond that, it gets confusing fast.

This post explains both methods in plain English, walks through a simple example so you can see the difference side by side, and covers why this question comes up more often in dental than in most other businesses.

How Cash Basis Works

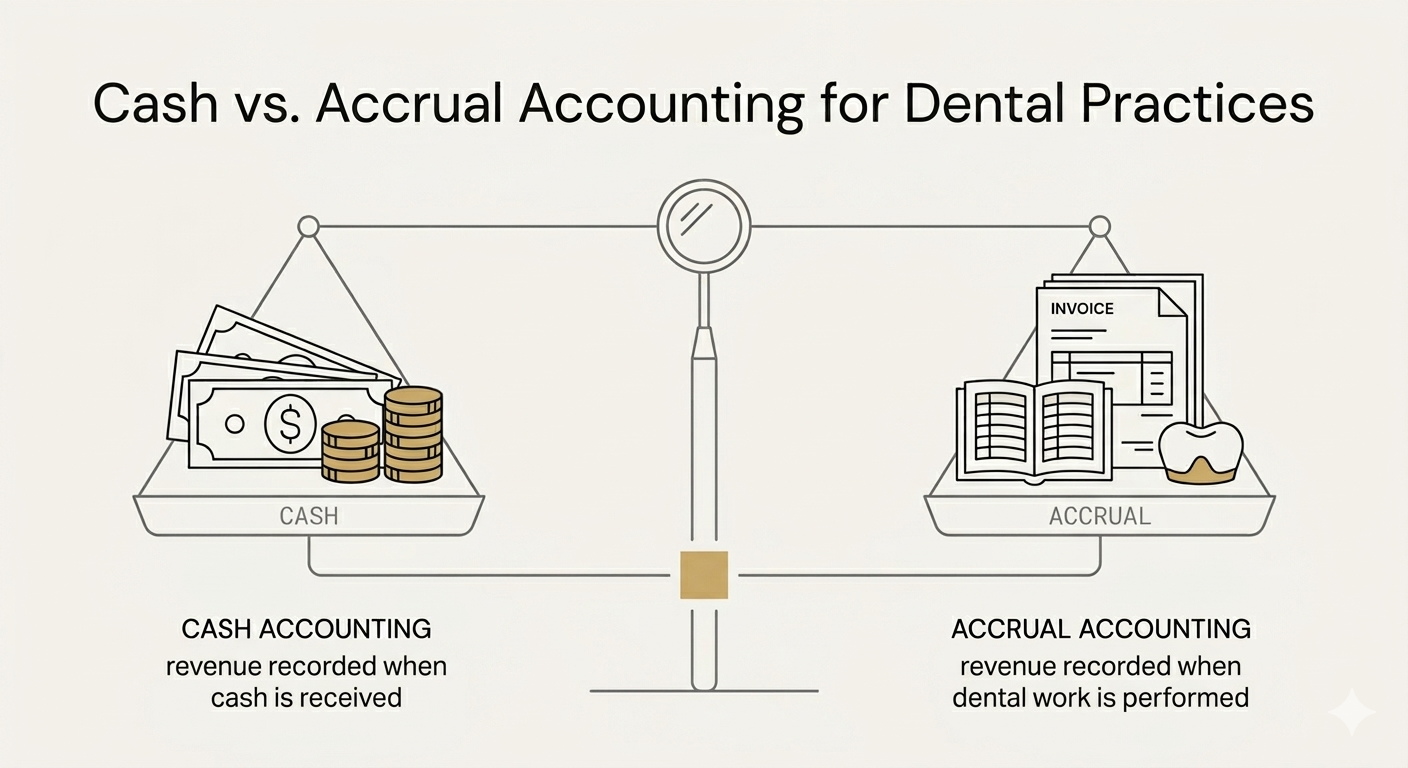

Cash basis accounting is straightforward: you record income when money hits your bank account, and you record expenses when money leaves. It doesn’t matter when you did the work. It only matters when the cash moved.

Here’s what that looks like in a dental practice:

You do a crown on March 5. Insurance pays on April 22. On cash basis, that revenue counts in April—the month the money arrived—not March, when the work happened.

A patient pays a $300 copay at checkout on March 5. That $300 is March revenue right away, because the cash came in that day.

Cash basis is common among small businesses and has been the default for many dental practices. It’s simpler to maintain, and if your bookkeeper is only working from bank deposits, it’s often the only method the data supports.

How Accrual Basis Works

Accrual basis accounting records income when you earn it and expenses when you incur them—regardless of when cash moves.

Same example: you do a crown on March 5. On accrual basis, the full value of that procedure—patient portion and expected insurance—is recorded as March revenue. When the insurance check arrives in April, it’s not new revenue. It’s a collection on revenue you already recorded.

Accrual gives you a more complete picture of any given month. Revenue matches the month the work was performed. Expenses match the month they were incurred. The timing of deposits doesn’t change the picture.

The Same Month, Two Different Numbers

Here’s a simple example to make this concrete.

Dr. Patel’s practice produces $100,000 in March. But the insurance payments that arrive in March are from February’s production, totaling $60,000. Patient copays collected at the front desk in March total $20,000. Expenses (supplies and payroll) for March are $40,000.

| Cash Basis | Accrual Basis | |

|---|---|---|

| Revenue | $80,000 | $100,000 |

| Expenses | $40,000 | $40,000 |

| Net Income | $40,000 | $60,000 |

Neither number is wrong. They’re answering different questions. Cash basis tells you what happened in your bank account. Accrual basis tells you what happened in your practice.

Why This Comes Up More in Dental

A coffee shop sells a drink and gets paid on the spot. There’s almost no gap between doing the work and getting the money, so cash and accrual would show nearly identical numbers.

Dental doesn’t work that way. A large share of revenue comes through insurance, which creates a lag of two to eight weeks between doing the work and receiving payment. Some claims take longer. Some get denied and resubmitted. Some involve coordination of benefits between two carriers.

That lag is what creates the gap between the two methods. On cash basis, your March financials don’t fully reflect March. They reflect a mix of February insurance payments and March copays. If a big batch of insurance checks happens to land in one month and not the next, your revenue swings—even if production was steady the whole time.

When you’re trying to answer questions like “Is my practice growing?” or “Was my new associate productive last quarter?”—cash basis numbers can be hard to read because they’re blending work from different months together.

The QuickBooks Toggle: Why It Doesn’t Do What You’d Expect

Most dental owners don’t know this, and many bookkeepers don’t mention it: the cash vs. accrual toggle in QuickBooks Online doesn’t do much for most dental practices.

That toggle only changes what you see if QuickBooks has the data to tell the difference between “revenue earned” and “revenue collected.” In most businesses, that data comes from invoices and accounts receivable entered as work is performed.

In a typical dental practice, QuickBooks doesn’t have that data. It only knows about deposits or money arriving in the bank. No invoices are created in QuickBooks when you do a procedure. No receivable is recorded.

So if you run a profit and loss on cash basis, you see deposits. Toggle to accrual, and you see the same deposits. There’s nothing else in the system to show you.

This isn’t a QuickBooks bug. The production data, what procedures were done, when, and for how much, lives in your practice management software (Open Dental, Dentrix, Eaglesoft). Until that data gets pulled into QuickBooks, the toggle has nothing to work with.

What Accrual Reporting Actually Requires

Getting a true accrual view of your practice means someone needs to pull production data from your practice management software and post it into QuickBooks on a regular basis. That gives QuickBooks two things it otherwise doesn’t have: what you produced and what you collected, as separate data points.

With that in place, your monthly financials show revenue based on work performed—not deposits received. The accounts receivable balance shows insurance claims that have been submitted but not yet paid. And the cash vs. accrual toggle in QuickBooks actually means something.

Without it, both views show the same deposit-based numbers.

This is the core difference between deposit-only bookkeeping and production-based bookkeeping. A deposit-only bookkeeper records what hits the bank. A production-based bookkeeper connects your practice management data to your accounting system so your financials reflect what’s actually happening in the practice.

Matching Your Books to Your Tax Return

Here’s something worth knowing: your tax filing method should match your bookkeeping method.

If your books track deposits only (cash basis), your tax return should be filed on cash basis. That’s consistent, and the numbers flow directly.

If your books track production and collections (accrual basis), your tax return should be filed on accrual basis. Everything lines up and no conversion needed at the end of the year.

Where it gets awkward is when the two don’t match. If your books are accrual but your taxes are cash, your tax accountant has to back out the accrual entries and recalculate a cash-basis number every year. It’s doable, but it’s extra work and extra cost for something that could be avoided by aligning the two methods from the start.

Switching Methods

If your practice has been filing on cash basis and you want to move to accrual (or the reverse), there’s an IRS process for that. Your tax accountant files a form with that year’s return, and there may be a one-time tax adjustment to account for income that was earned but hadn’t been taxed yet under the old method. For a dental practice, that’s typically the accounts receivable balance at the time of the switch—insurance claims submitted but not yet paid.

It’s a one-time step. After that, your books and taxes are aligned going forward.

For practices starting fresh—new practice, new bookkeeper, or a practice that never had production-based books before—there’s no switch to make. You pick your method from the beginning.

Talk to your tax accountant before making any change. They’ll walk you through the timing and the numbers.

Three Numbers Worth Knowing

If you take one thing from this post, it’s these three numbers:

Production is the dollar value of work you performed, measured on the date of service. It lives in your practice management software.

Collections is the money that actually arrived in your bank account—insurance payments, patient payments, CareCredit, membership plans. Collections always lag behind production because of insurance processing time.

Adjustments are the contractual write-offs between what you bill and what insurance actually pays. If you’re in-network with PPOs, these are built into your fee schedule. They’re normal, but they need to be tracked. Your net production (gross production minus adjustments) is the number to benchmark against.

A healthy collection rate—net collections divided by net production—runs between 98% and 100%. Below that, money is slipping through somewhere between the front desk and the bank.

Questions to Ask Your Bookkeeper

If you’re not sure how your books are set up, these are good questions to start with:

Are you pulling production data from our practice management software each month, or just recording deposits?

When I look at my monthly P&L, does the revenue line reflect what we produced or what we deposited?

Do we have accounts receivable tracked in QuickBooks?

Are our books on cash or accrual, and does our tax return match?

If your bookkeeper can’t answer these clearly, it doesn’t mean they’re doing a bad job. It may mean the scope of their work is deposit-only and nobody’s discussed it.

Frequently Asked Questions

Should my dental practice use cash or accrual accounting?

It depends on your situation and what you need from your financials. The most important thing is that your bookkeeping method and your tax method match. If your books are deposit-only, file cash. If your books track production and collections, file accrual. Your tax accountant can help you decide which method fits your practice. The key is consistency—pick one and align everything to it.

Can’t I just toggle QuickBooks between cash and accrual?

Only if QuickBooks has the underlying production data. Most dental practices enter deposits only, which means both views show the same numbers. The toggle becomes useful once production and accounts receivable are recorded in QuickBooks—which requires pulling data from your practice management software.

What is the difference between production and collections?

Production is the dollar value of work done at the chair, measured by date of service. It lives in your PMS. Collections is the money that actually arrives in your bank account, often weeks later after insurance processing. Deposit-only bookkeeping captures collections. Production-based bookkeeping captures both.

Why do my financials swing so much month to month?

If your books are deposit-only, your monthly revenue depends on when insurance payments arrive, not when you did the work. A big batch of payments in one month looks great; the next month looks flat—even if production was steady. Production-based reporting smooths this out by matching revenue to the month the work was performed.

What’s involved in switching from cash to accrual?

Your tax accountant files a form (Form 3115) with your tax return and handles a one-time adjustment (Section 481(a) adjustment) for any revenue that was earned but not yet taxed under cash basis. After that, your books and taxes are aligned going forward. It’s a one-time transition step, not an ongoing burden.

How much does accrual bookkeeping cost compared to cash basis?

Deposit-only bookkeeping typically runs $400–$800/month with a generalist. Production-based accrual bookkeeping runs $1,200–$3,500/month and includes pulling data from your PMS, posting production and collections, and delivering financials that reflect what happened in the practice. The price difference reflects a different scope of work, not just more hours.

You can see a full breakdown of the different service tiers and what a specialized dental bookkeeper typically includes in this post.

P.S. If you’re curious what production-based financials would look like for your practice, Reciprocity Accounting offers a free initial review of your current setup—no pitch, no pressure. Just a clear look at where things stand. reciprocityaccounting.com